MP Materials: Primed for Parabolic Surge by 2028?

Rare earth miner MP Materials positions itself as the Western world's answer to China's supply chain dominance—but can it deliver explosive growth within three years?

The Supply Chain Gambit

MP's entire thesis hinges on breaking China's stranglehold on rare earth elements. The company controls Mountain Pass—America's only active rare earth mine—giving it a geopolitical advantage that Wall Street can't ignore. With defense contractors and EV manufacturers desperate for non-Chinese supply, MP sits at the convergence of national security and green energy trends.

Execution Over Hype

While the narrative sparkles, the real test comes down to operational execution. MP must successfully scale its processing capabilities to capture full supply chain margins. The company's vertical integration strategy—from mine to magnet—could either create unprecedented value or become a capital-intensive nightmare. Recent quarterly results show progress, but the clock ticks toward 2028.

Market Forces at Play

Global rare earth demand projections look bullish, with electric vehicles and wind turbines driving consumption. MP's success ultimately depends on converting theoretical demand into contracted sales. The company faces pressure to secure binding off-take agreements before competitors establish alternative supply chains.

Parabolic potential exists, but requires flawless execution—something Wall Street analysts treat like a mythical creature spotted only during earnings season.

Image source: Getty Images.

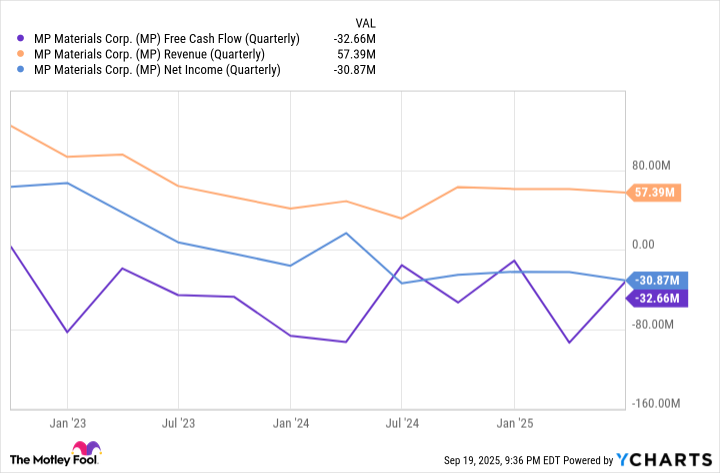

Strategic partnerships, but a cash-bleed problem

MP Materials makes money by selling rare-earth concentrates and oxides, like NdPr oxide, and by producing permanent magnets for a myriad of markets, including electric vehicles.

In July 2025, MP got two huge votes of confidence. One was a multibillion-dollar package from the Department of Defense (DoD), which invested $400 million in MP's stock and agreed to buy NdPr oxide at a price floor of $110 per kilogram over the next decade.

The second was a $500 million partnership with(AAPL 1.80%). A first-of-its-kind deal, MP will supply Apple with magnets for "hundreds of millions" of devices starting in 2027.

Both of these could set MP up for a strong three years to come. But let's not overlook the risks. MP isn't profitable, and it doesn't have the manufacturing capacity to meet high demand for super-strong magnets.

MP Free Cash FLOW (Quarterly) data by YCharts

At its current price, MP trades at almost 83 times forward earnings, a rich valuation that looks more like tech than mining.

With a multiple like that, MP will need something big -- like the completion of its 10X facility -- to go parabolic by 2028. It's possible, but only invest if you can stomach losses, as volatility should be expected.