William Blair’s Bold Call: Keep Buying Oracle Stock as the ’Key AI Beneficiary’

Wall Street's getting loud about Oracle's AI dominance—and one firm says the party's just getting started.

The AI Infrastructure Gold Rush

William Blair analysts are pounding the table on Oracle shares, labeling the tech giant the definitive winner in the artificial intelligence infrastructure race. Their thesis cuts through the market noise: enterprise AI adoption requires massive computing power, and Oracle's cloud architecture positions it as the backbone supplier.

Enterprise Adoption Accelerates

While startups chase flashy AI applications, Oracle quietly built the plumbing every Fortune 500 company needs. Their cloud infrastructure bypasses the consumer-facing hype to deliver the raw computational muscle required for serious AI deployment. Corporations aren't betting on chatbots—they're betting on Oracle's ability to handle their mission-critical data workloads.

The Analyst Conviction

This isn't some timid upgrade. William Blair's 'keep buying' recommendation comes with unusual conviction for a firm known for sober analysis. They see Oracle's enterprise foothold as an unbreachable moat—while smaller AI plays flash and crash, Oracle collects rent from the entire ecosystem.

Because nothing says 'sure thing' like a 45-year-old database company suddenly becoming Wall Street's hottest AI play. Sometimes the smartest trade is owning the picks and shovels instead of hunting for gold.

Elevate Your Investing Strategy:

- Take advantage of TipRanks Premium at 50% off! Unlock powerful investing tools, advanced data, and expert analyst insights to help you invest with confidence.

On Monday, the company unveiled a major leadership shift, with long-time CEO Safra Catz stepping aside as Clay Magouyrk and Mike Sicilia take over as co-CEOs. Magouyrk had been leading the OCI (Oracle Cloud Infrastructure) division, while Sicilia oversaw Oracle Industries, concentrating on vertical applications. During its business update call, management emphasized the scale of the AI opportunity across its operations and the unique advantages Oracle can deliver by integrating infrastructure, data, and applications. “Despite the management change,” says William Blair analyst Sebastien Naji, “we expect Oracle will remain on its current path, with the new co-CEOs doubling down on the AI theme and the company reaffirming its prior guidance.” Naji thinks more clarity on each executive’s strategic agenda will be forthcoming when Oracle hosts its AI World event next month.

Beyond the leadership shuffle, the Wall Street Journal reported yesterday that the U.S. and China are close to finalizing a deal on TikTok’s sale. The plan calls for a newly formed TikTok U.S. entity, with a consortium of investors led by Silver Lake and Andreessen Horowitz holding about half the stake, existing investors controlling another 30%, and parent company ByteDance retaining just under 20%. ByteDance WOULD license its algorithm to the new entity for use in a U.S.-specific app. Bloomberg added that Oracle is expected to provide the infrastructure needed to retrain and safeguard TikTok’s U.S. algorithm. For Oracle, this arrangement removes uncertainty about TikTok’s status as a customer, which Naji estimates accounts for $1–2 billion in annual revenue. “While there is still execution risk, with the potential shift to a new app and algorithm causing disruption and leading to user churn, we see an opportunity for Oracle to also substantially expand its revenue opportunity with the new U.S.-based entity,” Naji went on to add.

ORCL shares have been on a big runup recently, as the company hit a homerun in its recent quarterly report, with bookings having gone through the roof. But there’s no reason to step to the sidelines, says Naji. “While shares are not inexpensive, strong bookings growth points to a meaningful acceleration in Oracle’s revenue and earnings growth over the next several years,” the analyst opined.

Bottom line, with Oracle positioned as a “key AI beneficiary,” the set-up still looks favorable to Naji, who reiterated an Outperform (i.e., Buy) rating on the shares, with no fixed price target in mind. (To watch Naji’s track record, click here)

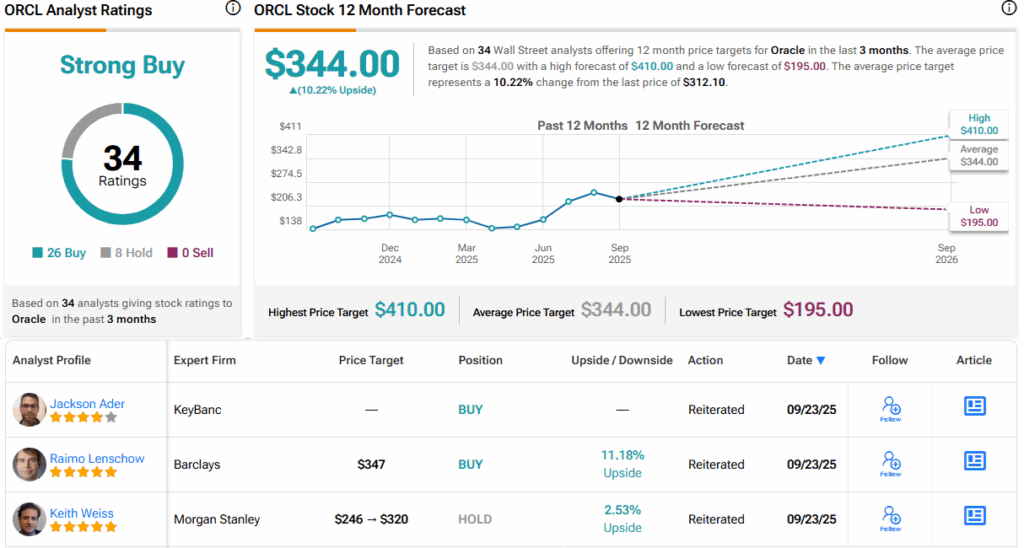

Others on the Street do have targets, and the average lands at $344, implying the shares will climb 10% higher in the months ahead. All told, the stock claims a Strong Buy consensus rating, based on a mix of 26 Buys and 8 Holds. (See ORCL stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.