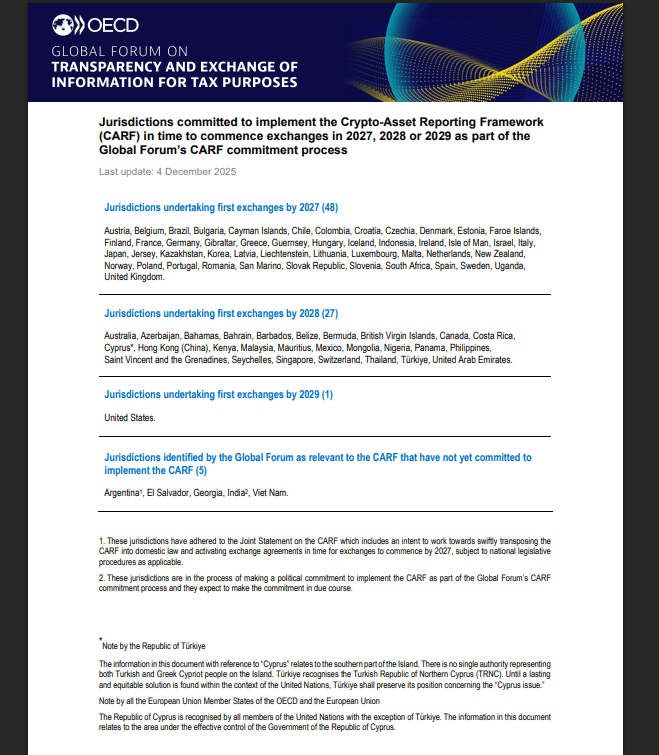

48 Nations Brace for 2027 Crypto Tax Crackdown: The Global CARF Era Begins

Get ready for a seismic shift in crypto oversight. Nearly fifty countries are gearing up to implement the Crypto-Asset Reporting Framework (CARF) by 2027, marking the most aggressive global tax coordination effort the digital asset space has ever seen.

The New Reporting Standard

Forget the old patchwork of national rules. CARF creates a unified playbook, forcing crypto exchanges and service providers to automatically report transaction data to tax authorities worldwide. It’s a direct response to the borderless nature of digital finance—governments are finally building a net wide enough to catch it.

What This Means for the Market

Expect operational overhead for businesses to spike. Compliance isn’t optional anymore; it’s baked into the global infrastructure. For users, the age of pseudo-anonymous cross-border trading is closing. Every transaction now has a potential paper trail leading straight to your local tax office.

The Institutional Green Light?

Paradoxically, this regulatory clarity could be the final stamp of legitimacy major funds have waited for. When the rules are clear—even if strict—big money tends to follow. It’s the ultimate ‘adult in the room’ moment, swapping wild-west chaos for monitored, reportable order. A necessary evil for trillions in institutional capital waiting on the sidelines, eyeing the space with a mix of greed and regulatory terror.

The bottom line: The crypto industry’s tax holiday is over. The 48-country coalition isn’t just watching anymore; they’re building the ultimate ledger. Compliance becomes the new mining rig—expensive, mandatory, and the only way to stay in the game. After all, nothing makes a traditional finance minister happier than finding a new asset class to tax.

Countries Begin Collecting Data

Based on reports, service providers such as major exchanges, some broker platforms, crypto ATMs and certain custody services will be obliged to record account details, transaction histories and users’ tax residency information for reporting to domestic tax authorities.

That information will be formatted so it can be shared automatically with partner tax offices once the exchange phase starts. The OECD monitoring update lays out the kinds of fields that must be gathered and stored for future reporting.

What Exchanges Must Report

According to news outlets tracking the rollout, exchanges are already adjusting onboarding forms and internal compliance systems to verify customers’ tax residency and capture wallet-level activity.

Some jurisdictions, led by the United Kingdom, have moved faster to require platforms to keep detailed purchase and sale records for users in scope. Tax authorities will then receive yearly reports covering balances, transfers and gains for listed accounts.

Operational Strain And Privacy QuestionsThe new rules create practical burdens. Smaller platforms will need to upgrade systems or hire compliance staff to track the new data points.

Based on reports, privacy advocates and parts of the crypto industry are warning that the depth of data collection could raise concerns about how long sensitive transaction records are held and who can access them.

Some legal teams are already studying how domestic data-privacy laws interact with automatic information exchange.

A further group of jurisdictions has said it will begin domestic collection later. Reports note that an additional 27 jurisdictions have timelines that target January 1, 2027 for starting to collect, with exchanges of information to follow in 2028 for that batch.

At least one analysis of national updates also indicates that a handful of countries are planning to stagger implementation because of local legislative calendars.

How This Will Play Out For UsersFor ordinary crypto users, the immediate change will be more questions during account setup and clearer record-keeping demands from providers.

Based on official guidance, CARF itself does not create new taxes; rather, it gives tax offices the data they need to enforce existing rules. For some investors, that means past reporting gaps will be easier for authorities to spot.

Reports have disclosed that implementation will vary by country. Some tax administrations are ready to receive standardized files in 2027, while others are still finishing domestic law changes.

Observers say the rollout marks a major step toward treating crypto transactions like other financial accounts when it comes to cross-border tax transparency.

Featured image from Unsplash, chart from TradingView